Platform

PLATFORM OVERVIEW

Your Money Line is an all-in-one financial wellness program that makes it easy for employers to offer personalized financial guidance to employees at every stage of life.

PLATFORM OVERVIEW

Your Money Line is an all-in-one financial wellness program that makes it easy for employers to offer personalized financial guidance to employees at every stage of life.

FEATURES

1:1 financial coaching

Smart budgeting & insights

Personalized money podcast

Credit monitoring

ID protection

Goals & assessments

Financial literacy education

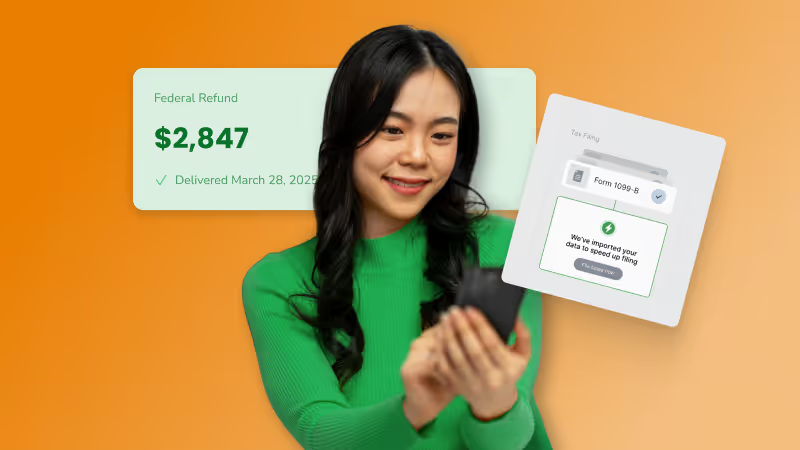

Tax filing

Who We Help

SOLUTIONS

Employers

We work with HR teams to round out your benefits

For Education

We guide teachers and staff to loan forgiveness & less worry

For Healthcare

We aid healthcare staff with financial planning & more

LEARN MORE

Success Stories

See how we're helping teams improve employee wellness

Wall of Love

Read real feedback from some of our clients and users.

Partners

Partner with us

Retirement Advisors

Differentiate your business with a leading financial coaching app

Benefits Brokers

Offer participants holistic wellness with a modern financial benefit

Pricing

Company

LEARN ABOUT YML

About

Learn about our mission, values, & the people who make it happen

Careers

We're hiring!

We’re always looking for stellar folks to join our team

News

Catch the latest YML news

Resources

2026 ANNUAL EMPLOYEE FINANCIAL BEHAVIOR REPORT

See what the latest data reveals about today’s workplace.

Download now

2026 ANNUAL EMPLOYEE FINANCIAL BEHAVIOR REPORT

Financial stress continues to weigh on employees’ focus, well-being, and performance. See what the latest data reveals about today’s workplace.

Download now

GROW WITH YML

Cha-Ching! Total Rewards Community

ROI Calculator

Money Vibe Quiz

learn

Blog

Resources

Newsletter

Watch a demo

Login

Blog Post

5 Alternatives to Smart Dollar: A 2026 Comparison of Financial Wellness Platforms

Kate Swack

January 26, 2026

This is some text inside of a div block.

This is some text inside of a div block.

Blog Post

Why Identity Theft Protection is an Important Employee Benefit

February 7, 2025

This is some text inside of a div block.

This is some text inside of a div block.

Blog Post

Why Baby Boomers Are Delaying Retirement—and What It Means for Employers

February 6, 2025

This is some text inside of a div block.

This is some text inside of a div block.

Blog Post

Financial Stress at Work: The Emotional Weight HR Can’t Afford to Ignore

January 24, 2025

This is some text inside of a div block.

This is some text inside of a div block.

Blog Post

Press Release

Download

Success Story

Webinar

Quiz

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Blog Post

Your Ultimate Guide to the 2026 SHRM Annual Conference

Kate Swack

May 5, 2026

This is some text inside of a div block.

This is some text inside of a div block.

Blog Post

February Financial Wellness Toolkit for the Workplace

Kate Swack

February 12, 2026

This is some text inside of a div block.

This is some text inside of a div block.

Blog Post

5 Alternatives to Smart Dollar: A 2026 Comparison of Financial Wellness Platforms

Kate Swack

January 26, 2026

This is some text inside of a div block.

This is some text inside of a div block.

Blog Post

January Financial Wellness Toolkit for the Workplace

Kate Swack

January 8, 2026

This is some text inside of a div block.

This is some text inside of a div block.

Download

2026 Financial Wellness Calendar for Employees

Kate Swack

December 22, 2025

This is some text inside of a div block.

This is some text inside of a div block.

Blog Post

Gen Z Financial Stress at Work: Causes and Solutions

Kate Swack

December 9, 2025

This is some text inside of a div block.

This is some text inside of a div block.

Blog Post

Why We’re Bringing Tax Filing to YML (and Why Your Employees Will Thank You)

Peter Dunn

December 8, 2025

This is some text inside of a div block.

This is some text inside of a div block.

Blog Post

Unlocking Financial Wellness ROI for Thriving Workplaces

Kate Swack

December 5, 2025

This is some text inside of a div block.

This is some text inside of a div block.

Blog Post

2026 Employee Benefits & Wellbeing Trends: What HR Leaders Need to Know

Kate Swack

December 3, 2025

This is some text inside of a div block.

This is some text inside of a div block.

Blog Post

The 2026 Guide to Measuring Workplace Financial Wellness Metrics

Kate Swack

December 1, 2025

This is some text inside of a div block.

This is some text inside of a div block.

Blog Post

How Much Do Financial Wellness Programs Cost? A Guide for HR Leaders

Kate Swack

November 24, 2025

This is some text inside of a div block.

This is some text inside of a div block.

Download

2026 Employee Benefits and Wellbeing Trends Playbook

Kate Swack

November 24, 2025

This is some text inside of a div block.

This is some text inside of a div block.

Load More

Huh, it doesn't look like we can find that for you. That's weird ಠ_ಠ

.jpg)

.jpg)

.png)

.png)

.avif)

.avif)

.avif)

.avif)

.svg)

.avif)